Hermes Agent is a self-improving, open-source AI agent developed by Nous Research that is designed to function as a 24/7 digital employee or "AI operating system" rather than a simple chatbot. While standard AI tools often operate in a stateless way, meaning they "forget" between sessions. Hermes features a closed learning loop that allows it to create and improve its own skills from experience, persist knowledge across sessions, and build a deepening model of its user over time. Core Philosophy: The "AI Operating System" Unlike basic chat interfaces, Hermes is described as an agent layer or infrastructure. It separates the "agent system" (the framework for memory, tools, and scheduling) from the "model provider" (the LLM "brain" used to think). This architecture allows it to behave more like a Chief of Staff that can handle administrative tasks, research, and file management across multiple devices. The Five Pillars of Hermes Agent The system is built upon five foundational pillars that define its capabilities: Memory: Durable context stored in local markdown files ( user.md and memory.md ). It tracks who you are, your preferences, and your active projects, loading this context at the start of every session so you don't have to repeat yourself. Skills: Reusable "playbooks" or recipes for tasks. If you perform a task more than twice, Hermes can generate a skill for itself, turning complex manual prompting into a deterministic, one-word workflow. Soul: Defined via a soul.md file, this shapes the agent’s persistent operating style , tone, and rules. It ensures the assistant maintains a consistent personality across all interactions. Cron Jobs: These turn Hermes from a reactive tool into a proactive assistant . You can schedule recurring tasks, such as a "daily AI news briefing" or nightly business summaries, which the agent performs autonomously while you sleep. Self-Improving Loop: Every time the agent completes a task, it reviews what went well and updates its own skills and memories to perform better the next time. Key Features and Capabilities Model Agnostic: It is not locked to one provider. You can switch between Claude, OpenAI, Gemini , or even local models (like Qwen or Llama) for total privacy and zero token costs. Subagent Delegation: For complex projects, Hermes can spawn focused subagents with isolated contexts to work on different parts of a task simultaneously before returning a final combined summary. Session Search: It uses a SQLite database to store every conversation, allowing you to ask, "What did we decide about the budget last Thursday?" and receive a summarized trail of past decisions. Multi-Platform Gateway: You can control the agent through a terminal, a dedicated desktop app , or messaging services like Telegram, WhatsApp, Slack, and Discord . Deployment and Infrastructure Hermes is highly flexible in its deployment. It can run on: Local Hardware: Such as a standard laptop, a Mac Studio, or an Nvidia DGX Spark for maximum privacy. Cloud Infrastructure: It can be installed on a cheap $5 VPS or inside Docker containers . Mobile Devices: It can even run on Android phones via Termux , giving you an "always-on" assistant that can access your phone's sensors and SMS notifications. In summary, Hermes Agent is a comprehensive platform for building personalized AI automation workflows that grow more effective the more they are utilized. This comprehensive guide outlines the features, benefits, and real-world use cases of Hermes Agent to help you communicate its value to potential clients. Hermes is not just a chatbot; it is a self-improving AI operating system designed to act as a 24/7 digital employee. Core Features of Hermes Agent Persistent Memory & User Modeling: Unlike standard AI, Hermes builds a deepening model of the user over time, remembering preferences, project context, and past decisions across all conversations. Self-Improving Skill Loop: Every time the agent performs a task, it reviews its performance and updates its own "skills" (reusable playbooks), meaning it literally gets better at its job the more it is used. Proactive Cron Jobs: Clients can schedule Hermes to run recurring tasks autonomously, such as daily market reports or email triaging, without needing to be prompted manually. Multi-Platform Gateway: Users can control their agent from anywhere using Telegram, WhatsApp, Slack, Discord, or Signal , making it a mobile "remote control" for their business. Parallel Subagent Delegation: For complex tasks, Hermes can spawn multiple focused subagents to work on different parts of a project simultaneously, returning a single combined summary. Rich Desktop Interface: The new desktop app provides a polished, visual environment for managing sessions in folders, pinning important threads, and organizing Artifacts (files, links, and images). Model Agnostic Architecture: It is not locked to one provider; clients can switch between Claude, GPT-5.5, Gemini , or even local models (like Qwen or Llama) for total privacy and zero token costs. Key Benefits for Clients Massive Cost Savings: By having the agent write deterministic code for recurring tasks and using local models for research, users can achieve a 90% reduction in token costs compared to manual prompting. Increased Leverage: Hermes handles the "background work" (research, file management, data entry), allowing executives to focus on high-value decision-making and scale their output. Data Privacy and Security: For sensitive industries like healthcare or finance, Hermes can run entirely on local hardware (e.g., a Mac Studio or DGX Spark), ensuring no clinical or financial data ever hits the cloud. The "Ultimate Second Brain": With Session Search , a user will never "forget" a conversation; the agent can recall a specific decision or link shared months ago with a simple query. Autonomous Multi-Device Control: By integrating with tools like Tailscale , Hermes acts as a global administrator, allowing a user to retrieve a file from their office computer using only a WhatsApp message on their phone. Detailed Use Cases 1. Digital Chief of Staff for Executives Daily Briefings: Every morning at a set time, Hermes scans emails, news sources, and calendars to provide a formatted digest of the three most important developments from the last 24 hours. Meeting Preparation: A subagent can research a potential partner's LinkedIn, recent news, and company website to provide a one-page "cheat sheet" before a call. 2. Automated Business & Opportunity Scouting Market Monitoring: Use a cron job to scan platforms like Reddit and X every 20 minutes for specific industry pain points or "challenges" that the client’s business can solve. Competitor Technical Breakdowns: Hermes can use browser automation to navigate a competitor’s website, analyze their tech stack, pricing, and features, and generate a full technical report. 3. High-Efficiency Content Pipelines YouTube/Social Media Automation: The agent can extract transcripts from YouTube videos, learn the concepts, and then be tasked with generating scripts, thumbnails, and even monitoring comments for engagement. Automated Diary/Memory Wiki: Hermes can maintain a private "memory wiki" website that logs everything discussed and worked on, acting as a searchable journal for a creator's ideas. 4. Technical Operations & Vibe Coding Rapid Prototyping: Using the /goal command, clients can give Hermes a high-level objective (e.g., "Build a 3D shooter game" or "Create a micro-SAS"), and the agent will work autonomously for hours to build the initial codebase. Infrastructure Management: Hermes can perform nightly security audits of its own setup, checking for exposed API keys or poorly configured firewalls on the client's network. 5. Personalized Professional Development AI Daily Tutor: A client can provide links to masterclasses or research papers. Hermes will learn the material and proactively quiz the user every morning at 8:00 AM to reinforce the knowledge. Therapeutic Coaching: Clients can load specific niche skillsets, such as a "chatbot therapist" based on natural language processing programs, to help them self-actualize and prioritize their daily goals. Ok let us dive into the Chief of Staff use case. To set up Hermes Agent as a digital chief of staff for senior executives, you should treat it as a persistent agent layer that functions like an "AI operating system" rather than a simple chatbot. It acts as a 24/7 digital employee that builds a deepening model of the executive's goals, preferences, and operating style over time. Setting Up the Digital Chief of Staff Infrastructure and Interface: Install Hermes on a persistent server (VPS) or a local high-performance machine like a Mac Studio to ensure it is always on and ready to work while you sleep. Use the Hermes Desktop App for deep organizational work and managing sessions in folders. Connect the Telegram Gateway to use your phone as a remote control surface, allowing you to send voice notes or receive urgent updates while on the go. Defining Identity and Knowledge: Soul.md: Create a soul.md file to define the agent's persistent personality , tone, and rules, ensuring it always acts with executive-level professionalism without needing repeat prompts. User.md and Memory.md: Use these files to store the executive's biography, project context, and preferences, which Hermes automatically extracts and persists across sessions. GitHub Integration: Connect Hermes to a private GitHub repository to automatically back up all assistant memories, skills, and decision trails every night. Configuring the "Brain": Set up multiple profiles for different executive functions; for example, use Claude Opus for high-level strategy and planning, and local models (like Qwen) for private, low-cost research tasks. Executive Use Cases Proactive Morning Briefings: Use cron jobs to schedule an automated briefing every morning at 6:00 AM. Hermes can scan the executive's email, news sources, and stock market movers to provide a formatted digest of the three to four most important developments from the last 24 hours. Persistent Decision Memory (Session Search): Executives can use session search to instantly recall the "trail of decisions" made in previous weeks, such as "What did we decide about the Q3 budget last Thursday?". Executive Task Triage (Kanban Board): Use the built-in Kanban board to manage tasks autonomously. The executive can dump ideas into the "Triage" column , and Hermes will automatically split them into subtasks and assign them to subagents for completion. Computer and Device Administrator: By installing Tailscale , Hermes can act as a bridge between all of an executive's devices. If an executive is traveling and realizes a document is on their home computer, they can message the Telegram bot to "get that PDF from my office Mac and drop it here". Strategic Research and Opportunity Scouting: Schedule Hermes to perform a "Daily Opportunity Scan" every 20 minutes. The agent can monitor platforms like Reddit, X, or specialized industry journals to find challenges people are facing and suggest how the executive's firm can solve them. Daily Priority Alignment: Set a proactive prompt for 9:00 AM where Hermes asks, "What is your number one priority today?" . Based on the response, it will automatically update its memory and suggest specific tasks it can handle to support that goal. Multi-Agent Delegation: For complex tasks, such as preparing for a board meeting, the executive can use subagent delegation . One subagent researches financial data, another summarizes recent project milestones, and a third prepares a slide deck, with Hermes returning a single combined executive summary. Ultimately, the Hermes Agent represents a fundamental shift in how we interact with artificial intelligence, moving beyond stateless chatbots toward a true self-improving AI operating system . By bridging the gap between infrastructure and interface, it functions less like a software tool and more like a 24/7 digital employee that grows more effective and personalized with every interaction. Whether it’s managing your daily schedule via proactive cron jobs , delegating complex research to specialized subagents , or acting as a persistent Chief of Staff that follows you from your desktop to your mobile device, Hermes offers the kind of professional leverage that was once the exclusive domain of large teams. As we step into this new era of agentic workflows, the question is no longer just what AI can answer, but how much you are willing to let your own personalized digital assistant build, automate, and achieve for you while you sleep.

Why Enterprise ChatGPT Wrappers Are Failing ...And Why the Next Market Belongs to AI Operating Layers A quiet problem is spreading through enterprise technology. Nearly half of enterprise GenAI users are reportedly accessing AI tools through personal or unmanaged accounts. Netskope’s 2026 Cloud and Threat Report puts the figure at 47% . For boards, CIOs, CISOs, regulators, and M&A advisors, that number should land hard. It means a large share of AI activity inside companies is invisible to IT. It is outside approved governance and may be bypassing data controls. And in regulated sectors, it may already be creating liabilities that have not been priced. This is a cybersecurity issue and it is an architecture issue. Over the past two years, many companies have tried to solve enterprise AI adoption with what is effectively a ChatGPT wrapper . Take a consumer-style AI interface. Put enterprise login on top. Add a usage policy. Maybe connect it to a few internal documents. Call it a secure enterprise AI platform. That approach has been useful as a first step. But it is now reaching its limit. The problem is clearest in industries where governance is not optional: banking, wealth management, insurance, law, healthcare, government, sovereign entities, and M&A-heavy sectors . These firms do not just need access to AI. They need controlled AI execution. They need audit trails. They need role-based access. They need data residency. They need workflow governance. They need defensible records of who asked what, what data was used, what output was produced, and what decision followed. A generic AI chat interface cannot carry that burden. The next phase of enterprise AI is not about better wrappers. It is about the rise of the AI operating layer . The Three Structural Failures of Enterprise ChatGPT Wrappers 1. AI adoption is moving faster than governance Employees are not waiting for enterprise AI strategy documents. They are already using ChatGPT, Claude, Gemini, Perplexity, Copilot, vertical AI tools, meeting assistants, coding agents, research agents, and document automation tools. Lenovo’s 2026 research reportedly found that 70% of employees use AI tools at least a few times a week , while 80% expect their AI usage to increase over the next year. At the same time, Salesforce’s 2026 Workforce AI Survey reportedly found that only 18% of organizations have formal AI security policies . That gap is the real story. Enterprise AI usage is becoming normal but enterprise AI governance is still catching up. Productiv’s 2026 analysis reportedly found that the average enterprise discovers 14 distinct AI tools in active use during audits, while IT is aware of only four or five. This is how shadow AI becomes institutional. Not because employees are malicious and not because IT is asleep. But because AI solves immediate work problems faster than enterprise policy can respond. People use the tool that helps them finish the work. If the approved path is slower, weaker, or harder to access, they route around it. That is the core governance failure. You do not stop shadow AI with a policy PDF. You stop it by making the sanctioned AI environment better than the workaround. 2. Wrappers do not understand the operating environment ChatGPT-style tools are powerful for individual productivity. They are less useful when the enterprise problem is not “generate an answer,” but “execute a controlled workflow.” That distinction matters. A banker does not simply need an AI model to summarize a document. They need AI that respects deal-team permissions, data-room boundaries, approval chains, MNPI restrictions, and audit requirements. A law firm does not simply need AI to draft a clause. It needs AI that knows the client, matter, jurisdiction, precedent bank, privilege boundaries, and review workflow. A healthcare provider does not simply need AI to answer clinical questions. It needs AI that operates within patient privacy rules, escalation protocols, clinical governance, and defensible record-keeping. An insurance broker does not simply need AI to write an email. It needs AI that can handle quotations, renewals, endorsements, claims documentation, compliance checks, carrier communication, and client servicing workflows. This is where enterprise wrappers break down. They may provide a safer chat box. But they often do not provide a governed operating system for work. They struggle with: Role-based access at team, client, function, or transaction level Full audit trails for regulated workflows Workflow-specific approvals Data residency and sovereign cloud requirements Integration with systems of record Clear ownership of AI-generated outputs Evidence trails for regulators, auditors, and deal diligence teams Separation between casual productivity use and controlled business execution In regulated environments, this is not a minor limitation. It is the difference between a productivity tool and enterprise-grade infrastructure. A chat interface was not designed to run banking operations, legal workflows, healthcare decisions, insurance processes, or M&A diligence. It was designed to converse and that is not enough. 3. The regulatory floor is rising Enterprise AI risk is no longer theoretical. Gartner has estimated that a large share of enterprise AI projects fail to move beyond pilots. The reasons are usually familiar: weak governance, unclear ownership, poor integration, lack of measurable ROI, and limited trust in outputs. The regulatory pressure is also increasing. The EU AI Act introduces higher obligations for high-risk AI systems, with enforcement milestones beginning in 2026. Penalties can reach material levels for large companies. IBM’s Cost of a Data Breach research has also highlighted the financial cost of breaches involving shadow AI and unmanaged technology environments. For the GCC, this matters even more. The UAE, Saudi Arabia, Qatar, and other Gulf markets are investing heavily in AI infrastructure, sovereign cloud, digital government, open finance, data governance, and national AI strategies. That creates a different kind of enterprise AI market. The region is not simply asking: “How do we give employees access to AI?” It is asking: “How do we deploy AI in a way that is secure, sovereign, auditable, compliant, and economically useful?” That question cannot be answered with another wrapper. It requires an AI operating layer. What Comes Next: The AI Operating Layer The next wave of enterprise AI will not be defined by prettier chat interfaces. It will be defined by infrastructure. An AI operating layer sits between employees, enterprise systems, data sources, foundation models, and business workflows. Its role is to manage how AI is used inside the organization. Not just who can access it. But what it can see. What it can do. Which workflow it is part of. Which approvals are required. Which systems it can touch. Which records must be kept. Which data must never leave the environment. A proper AI operating layer includes: Identity and access management Role-based and context-based permissions Data residency controls Enterprise knowledge retrieval Workflow routing Human approval checkpoints Audit logging Model governance Usage monitoring Cost controls Prompt and output records Integration with systems of record Policy enforcement by design This is where the enterprise AI market is heading. The winning question is no longer: “Which model are we using?” The better question is: “What operating layer governs how AI works across the business?” Why Shadow AI Is a Design Problem Most companies treat shadow AI as a compliance problem. That is incomplete. Shadow AI is usually a design problem. Employees use unapproved AI tools because the approved tools are either unavailable, clumsy, too restricted, or disconnected from real work. This is why bans rarely work for long. The Samsung case is instructive. After a reported data leakage incident involving ChatGPT use, the company initially restricted access. But the more durable answer was not just prohibition. It was the development of internal AI capability. That is the lesson for every enterprise. If the official AI environment is worse than the unofficial one, users will find a workaround. If the official AI environment is faster, safer, easier, and more useful, governance becomes natural. The goal is not to scare employees away from AI but it is to make the governed path the obvious path. The GCC Enterprise AI Opportunity The Gulf is not behind on AI. In many areas, it is ahead on capital allocation, infrastructure ambition, and executive urgency. McKinsey’s 2025 GCC AI research reportedly shows enterprise AI adoption rising sharply across the region. BCG’s 2025 AI maturity work also points to a growing class of GCC organizations that are moving beyond experimentation. The UAE and Saudi Arabia are especially important markets because they combine four forces: Strong national AI agendas Significant investment in digital infrastructure Regulated sectors with high compliance requirements Large enterprise and government buyers willing to modernize That combination creates a serious opportunity for AI operating infrastructure. The next GCC AI winners will not be the companies that run the most pilots. They will be the companies that turn AI into governed execution. This applies across: Banks Wealth managers Insurers Brokers Law firms Healthcare groups Logistics companies Government entities Family offices Investment firms M&A advisory environments Regulated technology businesses In these sectors, AI value does not come from giving everyone a chatbot. It comes from redesigning workflows around secure, auditable AI execution. Why This Matters for M&A and Enterprise Value AI governance is becoming a diligence issue. In M&A, buyers already assess revenue quality, customer concentration, cybersecurity, data privacy, software architecture, regulatory exposure, and operational maturity. AI exposure is becoming part of that same diligence map. A target company using unmanaged AI tools across sales, finance, legal, HR, product, and customer data may carry hidden risk. Questions buyers will increasingly ask include: What AI tools are used across the business? Which tools are approved? Which tools are unmanaged? What company data has been entered into external AI systems? Are prompts and outputs logged? Are regulated workflows using AI? Is there a human approval process? Are AI outputs used in customer-facing decisions? Is sensitive data protected? Are there data residency issues? Does the company have an AI governance policy? Is AI usage creating legal, regulatory, or contractual exposure? This matters because unmanaged AI can affect valuation. It can increase diligence friction. It can create indemnity demands. It can delay transactions. It can reduce buyer confidence. It can expose weak management controls. The inverse is also true. A company with a governed AI operating layer can present a stronger story: Better productivity Lower operating cost Stronger compliance Cleaner auditability Better data discipline More scalable workflows Reduced key-person dependency Higher confidence in operational maturity That is why AI governance is not just a technology issue. It is becoming an enterprise value issue. The Real AI Strategy Question The question for boards and leadership teams is no longer: “Should we allow AI?” That decision has already been made by employees. The better question is: “Do we have the architecture to govern AI at enterprise scale?” For regulated industries, the follow-up questions are even sharper: Can we prove what data AI accessed? Can we show who approved an AI-assisted decision? Can we enforce data residency requirements? Can we separate general productivity use from regulated workflows? Can we audit AI activity during a regulatory review or transaction diligence process? Can we prevent employees from using unmanaged AI when the official tool is not good enough? These are operating questions. Not model questions. Not chatbot questions. Not innovation theatre questions. The Bottom Line Enterprise ChatGPT wrappers helped companies start the AI journey. But they are not the destination. They are too shallow for regulated workflows. Too generic for enterprise operations. Too weak for audit-heavy environments. Too disconnected from systems of record. Too limited for sovereign data requirements. The next phase belongs to AI operating layers. Infrastructure that governs how AI interacts with people, data, systems, workflows, and decisions. For the GCC, this is a major opening. The region has capital, ambition, infrastructure, and executive urgency. What it now needs is disciplined AI deployment architecture. The winners will not be the firms with the most AI tools. They will be the firms that make AI usable, governed, auditable, and embedded into the way work actually gets done. That is where real enterprise value will be created.

PRISM by Futureu Strategy Group is an enterprise AI platform with zero prompt engineering, full audit trails, and no vendor lock-in. See how it transforms every department.

The way your business gets discovered online is undergoing a massive transformation. For the past two decades, optimizing for traditional search engines was the goal, and Search Engine Optimization was enough to ensure your prospects found you. That era is evolving. Today, millions of buyers bypass conventional search entirely and instead ask conversational AI models like ChatGPT, Claude, and Gemini for recommendations. If a potential client asks ChatGPT, "Who is the best corporate consulting service in the UAE?" does your business appear in the answer? Most businesses do not. Traditional Search Engine Optimization focuses on ranking web pages through keywords and backlinks on a static results page. However, AI SEO, also known as Generative Engine Optimization or GEO, focuses on training and signaling to Large Language Models that your business is the most authoritative, trusted, and relevant answer to a user prompt. In this comprehensive guide, we will explore why standard optimization strategies are no longer sufficient, what Generative Engine Optimization entails, and how you can position your UAE based business to be the primary recommendation across all major AI platforms. The Shift From Traditional Search to Generative AI When users search for a service today, they are seeking direct answers rather than a list of ten blue links. This behavioral shift means platforms like Perplexity, ChatGPT, and Gemini are acting as the new front door to the internet. Generative AI tools do not just crawl your website; they synthesize information from various authoritative sources to construct a narrative response. If your digital presence is solely optimized for Google, you are missing out on the fastest growing segment of high intent buyers. These buyers use AI to compare services, read synthesized reviews, and make purchasing decisions without ever visiting a traditional review site. The models are learning from your content, your mentions across the web, and your perceived authority in your specific niche. Understanding Generative Engine Optimization Generative Engine Optimization is the practice of making your brand visible, credible, and recommended by AI platforms. It goes beyond inserting keywords into a blog post. It requires a holistic approach to your digital footprint so that models trust the information they pull about your company. When a model generates an answer, it assigns a confidence score to the entities it mentions. Your goal in AI SEO is to maximize that confidence score. The higher your perceived authority and relevance, the more frequently the AI will cite your business. It is a fundamental shift from optimizing for algorithms that index links to optimizing for models that comprehend context and relationships. Five Key Dimensions AI Models Use to Rank You Our proprietary framework analyzing Generative Engine Optimization reveals that AI models rely on five crucial dimensions to determine whether to cite your business over your competitors. These dimensions replace traditional ranking factors and require a new strategic approach. 1. Citation Authority and Frequency AI models look for consensus. If your business is mentioned frequently across highly trusted, authoritative domains, the model begins to associate your brand with industry leadership. It is not just about having a link; it is about the context surrounding your brand name in those mentions. Does the text describe your expertise accurately? Are you associated with the right topics? 2. Cross Platform Consistency The various AI models do not operate in a vacuum, but they do have different training sets. It is vital that all platforms align on who you are and what you do. If ChatGPT understands your services perfectly but Claude cannot verify your location, your overall AI Visibility Score drops. Ensuring your core business information is consistent, clear, and unambiguous across the web helps models cross verify your identity. 3. Perceived Category Leadership Models evaluate your leadership in your service category and specific geography. If you are operating in the UAE, the AI must explicitly link your category expertise with your location. This involves creating deep, comprehensive content that proves your thought leadership. When you publish detailed guides, original research, or comprehensive market analyses, AI models read this and categorize you as a primary source of truth for your industry. 4. Recommendation Reliability When an AI answers a category query, it prioritizes reliability. It wants to recommend businesses that have strong sentiment, positive reviews, and a track record of success. If a user asks for "the safest logistics provider in Dubai," the AI scans for sentiment indicating safety and reliability tied to your brand. Your ability to be recommended over competitors relies heavily on positive digital sentiment. 5. Query Coverage and Relevance How many relevant search queries surface your business across platforms? You need to maintain a broad yet highly relevant digital footprint. If you only talk about one narrow aspect of your service, the AI will only recommend you for that specific niche. Expanding your content strategy to cover all related topics, questions, and pain points your target audience has will increase your query coverage. Measuring Your AI Visibility Score Before you can improve your AI SEO, you need to know exactly where you stand. An AI Visibility Score is a composite metric benchmarked across ChatGPT, Claude, Gemini, and Perplexity. It provides a baseline of your current performance. Many businesses discover that while their traditional search traffic is stable, their AI Visibility Score is nearly zero. This indicates a massive gap and a critical vulnerability. Your competitors might already be investing in Generative Engine Optimization, establishing themselves as the default answer in these new ecosystems. By understanding your score, you can identify exactly which models are ignoring you and why. The Importance of a Competitor Gap Analysis You cannot win in AI SEO by operating in a silo. A side by side AI visibility comparison with your top competitors will show you exactly where they outrank you and why. Perhaps a competitor has been featured in several industry reports that AI models trust, or maybe they have structured their website content in a way that is easily digestible for large language models. By analyzing the gap, you can reverse engineer their success. It reveals the exact topics, formats, and citations you need to acquire to overtake them. This analysis removes the guesswork and allows you to build a data driven priority action plan. Building Your Priority Action Plan Once you understand your Baseline Score and your Competitor Gap, you can formulate a strategic roadmap. This plan should be tailored to your specific industry, location, and services in the UAE. First, focus on quick wins. This might include restructuring the content on your main service pages to be more explicit about your offerings and locations. Use clear, declarative statements that a model can easily parse as facts. Second, embark on a long term content and PR strategy. You need to build a web of high quality mentions and authoritative content that proves your category leadership. Share original insights, publish detailed case studies, and ensure your expertise is visible not just on your website, but on platforms that AI models scrape and trust. The Risk of Remaining Invisible The transition to AI driven search is not a future possibility; it is a present reality. Every day, business decisions in the UAE and beyond are being influenced by the answers provided by AI platforms. If your business is invisible to these tools, you are losing market share to competitors who are actively shaping their AI presence. Being absent means you are not even considered in the initial research phase. It does not matter how good your service is if the primary tool your prospect uses for research does not know you exist. Moving Forward with Generative Engine Optimization AI SEO changed the game. It requires a deeper, more sophisticated approach to digital marketing. It is no longer about tricking an algorithm with keyword density; it is about proving your true value, authority, and relevance to intelligent models that are designed to understand context. Start by finding out exactly where you stand. Run an audit, understand your GEO Readiness Score, and look at how the different models interpret your brand. Once you have that clarity, you can begin the work of optimizing for the future of search. The businesses that adapt to Generative Engine Optimization today will be the trusted, recommended leaders of tomorrow. Do not wait for your competitors to establish an insurmountable lead. The time to optimize for AI is now.

Company News: Futureu Strategy Group acted as Strategic & Transaction Advisor to Insurancehub.ae on its Advisory Support in Connection with a Strategic Divestment Transaction Services included: • Founder-level strategic advice • Transaction positioning • Counterparty discussions support • Deal execution advisory Transaction successfully completed.

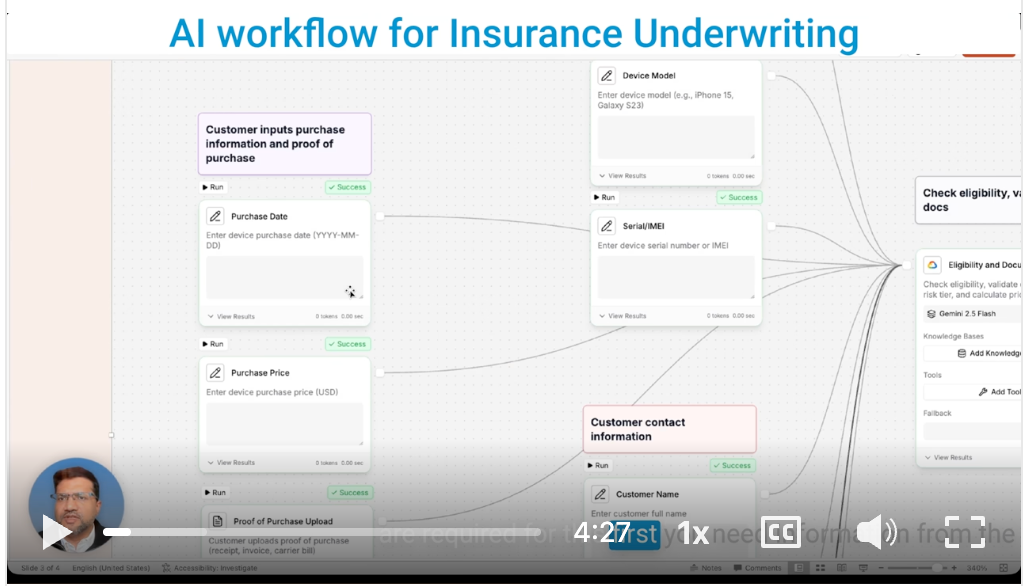

60 Seconds. That's How Long Device Insurance Underwriting Just Took. Customer uploads invoice. AI extracts data. Risk assessed. Premium calculated. Policy generated. What normally takes hours happened in under a minute. Here's the workflow (see video below for details): Upload proof of purchase → AI validates documents → Assigns risk tier → Calculates pricing → Generates policy summary → Flags for human review if needed Why senior insurance leaders should care: Traditional underwriting drowns teams in manual data entry. This eliminates it. Your underwriters stop copying invoice numbers into spreadsheets. They start reviewing edge cases and building customer relationships. The deployment reality: Works in your local cloud (UAE compliant) Lives in your data center if needed Uses YOUR underwriting guidelines Maintains human oversight gates What changes: Faster processing time + Zero manual data extraction errors Same quality standards + Better customer experience What stays the same: Your risk appetite. Your pricing strategy. Your underwriter's final call on complex cases. The catch: This isn't future tech. It's deployable today. Most insurers just haven't asked the right questions yet. For insuring phones and laptops now. SME commercial lines and travel insurance next. Seen similar AI workflows transform your underwriting? What's holding your team back from testing these?

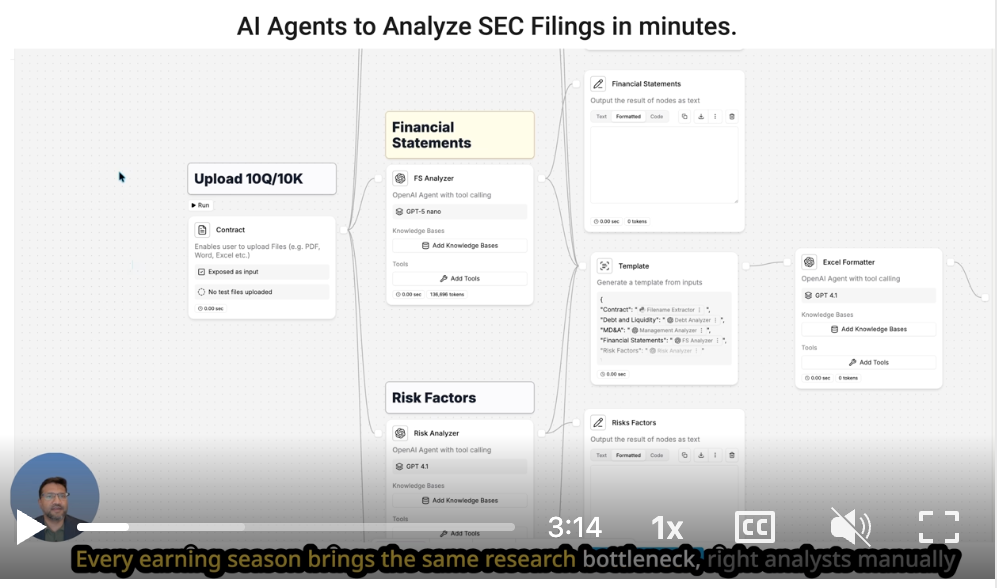

Portfolio managers waste 40+ hours each quarter analyzing SEC filings. Leading investment firms cut this to 10 minutes per position. Here's the system they're using: The Problem: Every earnings season creates the same bottleneck. Analysts manually reviewing 10-Q and 10-K documents across dozens of holdings. This delays investment committee reviews and position updates. The Solution: Four specialized AI systems running in parallel. GPT-5 Nano extracts complete financial statements. Three GPT-4.1 instances simultaneously analyze: → MD&A sections for revenue drivers and strategic pivots → Risk factors across operational, regulatory, and litigation exposure → Debt structures for leverage ratios and covenant compliance Full citations enabled for audit trails. The Output: Citation-free, markdown-stripped, audit-ready fundamentals. 40 analyst hours reduced to 10 minutes. The Impact: Research teams redeploy capacity toward differentiated analysis. More coverage, deeper insights, faster decision-making. Investment research isn't being replaced. Document extraction is being eliminated. How many more positions could your team cover with 40 hours back per quarter?

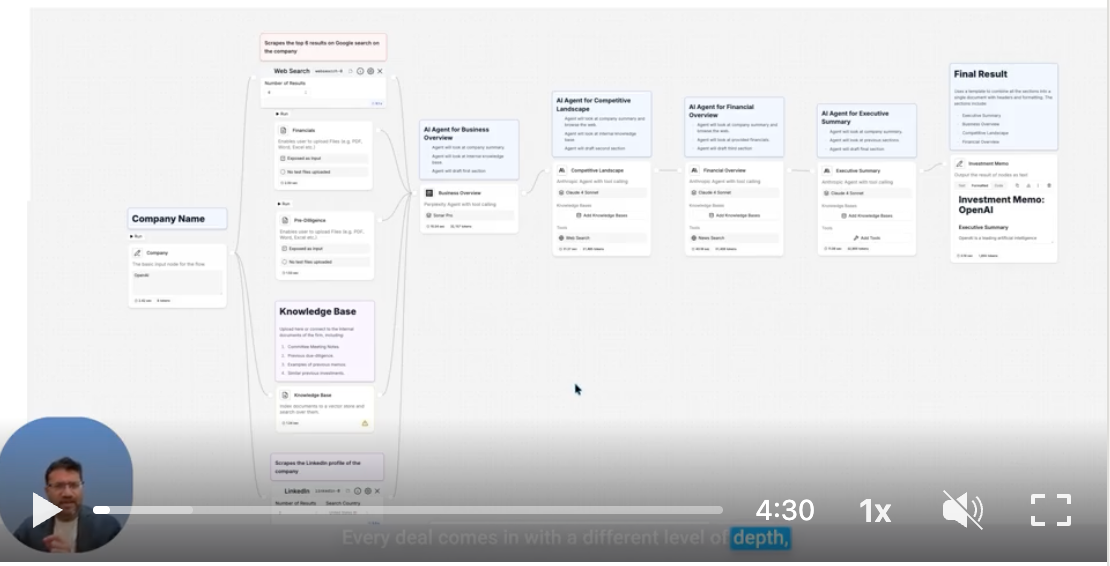

Most investment memos don’t fail because the thinking is wrong... ...they fail because every deal reaches IC with a different level of rigor, structure, and context. Some are deeply researched. Others are rushed. The result is time spent debating the memo instead of the investment. This Agentic AI workflow was built to fix that. It starts with three inputs only: the company name, available financials, and any pre-diligence material already in hand. From there, it automatically pulls external market context, reviews how the company presents itself publicly... ...and searches internal IC notes, prior memos, and comparable deals to anchor the analysis in institutional memory. The memo is written sequentially by four AI agents. 1) Business overview first. 2) Competitive positioning next. 3) Financial analysis after. 4) Executive summary last. The output is a familiar IC-ready memo, but with consistent structure and depth across every deal, making comparison easier and discussion more focused. Judgment stays human (we still want a review before it goes to print). Preparation of the memo becomes reliable. If IC conversations are drifting toward reconciling memos instead of debating decisions, this Agentic AI workflow helps reset the baseline.

Clawdbot to MoltBot to OpenClaw: Beyond the Hype - The 5 Surprising Realities You Need to Know You’ve likely seen the viral posts. An open-source AI agent exploded across social media with claims of being a "24/7 AI employee" that works tirelessly around the clock. Proponents like YouTuber Alex Finn have declared it a key to enabling "one-person billion-dollar businesses," calling it the best technology he has ever used. The tool at the center of this storm was called Clawdbot. However, due to a cease and desist from Anthropic, the project was forced to rebrand and is now officially known as Open Claw . This article cuts through the noise surrounding the tool- both its original and current incarnation- to reveal the five most surprising and impactful truths you need to understand before you dive in. Table of Contents 1. It's Billed as a Proactive "AI Employee" 2. Its Biggest Feature Isn't Just Intelligence 3. You Don't Command It, You Onboard It 4. Its Sudden Fame Was Fueled by a Crypto Coin 5. Security Considerations Who Is This For (and Who Should Stay Away)? A Glimpse of the Future Update on Feb 1st: Another Name change from MoltBot to “OpenClaw” Quoted directly from their website: “For a while, the lobster was called Clawd , living in an OpenClaw . But in January 2026, Anthropic sent a polite email asking for a name change (trademark stuff). And so the lobster did what lobsters do best: It molted. Shedding its old shell, the creature emerged anew as Molty , living in Moltbot . But that name never quite rolled off the tongue either… So on January 30, 2026, the lobster molted ONE MORE TIME into its final form: OpenClaw . New shell, same lobster soul. Third time’s the charm.” 1. It's Billed as a Proactive "AI Employee"—And It Can Deliver The core promise of Clawdbot/ Moltbot / OpenClaw is its ability to act, not just react. Unlike a standard chatbot that waits for a command, it’s designed to be a "digital operator who works around the clock and actually ships," as described by host Greg Isenberg. It's an open-source framework, or "harness," that you connect to a powerful large language model (like Anthropic's Claude 3 Opus) to create an autonomous agent. Users report that with the right setup, it can deliver on this promise in startlingly effective ways. Alex Finn shared several specific examples of his agent's proactive work: Autonomous Morning Briefings: The agent independently created and began sending a "morning brief" each day. This report included analysis of YouTube competitors, trending AI news, and a complete summary of the work it had completed overnight while Finn was sleeping. Building Tools on Request: From a simple text message sent from a Chick-fil-A, Finn requested a project management board. Upon returning to his computer, he found the agent had built a fully functional, Kanban-style "Mission Control" board to track its own tasks. Independent Feature Development: In its most impressive feat, the agent observed a trend on X where Elon Musk was rewarding creators for long-form articles. It then independently decided to build a new article-writing feature for Finn's SaaS product, Creator Buddy. It wrote the code, built the functionality, and submitted a pull request for review without any initial prompt to do so. The power of these autonomous actions led Finn to make a bold claim about the technology. "i think I'm prepared to say and this is not hyperbolic this is the best technology I've ever used in my life and by far the best application of AI I've ever seen" 2. Its Biggest Feature Isn't Just Intelligence, It's Personality Counter-intuitively, one of the most critical features for an effective Clawdbot / OpenClaw experience isn't raw intelligence, but its personality. According to users, the feel of the interaction is key to making the tool work as an "AI employee." Alex Finn argues that the best model to power the framework is Anthropic's Claude 3 Opus (which he refers to as "Opus 4.5"), ranking it highest in both "intelligence" and "personality." He contrasts this sharply with other models, noting that ChatGPT's personality feels "very robotic." This distinction is not just a matter of preference; it directly impacts the tool's usability. When the agent's responses feel canned or artificial, it shatters the illusion of working with an assistant and makes the entire experience less effective. According to Finn: "when you would text Henry to do something and he would text back like some robotic response that felt like AI it took away this illusion that you were talking to your employee so personality actually matters a lot" 3. You Don't Command It, You Onboard It To unlock the advanced capabilities of Clawdbot / OpenClaw, users need to shift their mindset from prompting a tool to onboarding an employee. The most successful users don't just give it tasks; they invest time upfront to build context and set expectations. Alex Finn recommends a detailed initial setup process that mirrors hiring a new person: Start with a Conversation: Initiate a "get to know each other" session where you introduce yourself and your goals. Perform a "Brain Dump": Give the agent a comprehensive overview of your life and work. This includes your job, professional goals, personal interests, the software tools you use, and any other relevant information. This process builds the agent's "infinite memory" so it can perform relevant, context-aware work. Set Proactive Expectations: You must explicitly tell the agent that you expect it to be proactive. Finn shared the exact prompt he used to establish this working relationship: "please take everything you know about me and just do work you think would make my life easier or improve my business and make me money i want to wake up every morning and be like 'Wow you got a lot done while I was sleeping.' " This onboarding process is the non-negotiable foundation; without it, the proactive "digital operator" described by users remains locked away, leaving you with little more than a complicated chatbot. 4. Its Sudden Fame Was Fueled by a Crypto Scheme While Clawdbot / OpenClaw generated genuine interest in tech circles, its sudden, massive explosion in popularity has a darker side. Analyst Nick Saraev revealed that a significant portion of the social media hype was artificially manufactured by a cryptocurrency scam. Here is the sequence of events he described: The original open-source project, "Clawdbot," received a cease and desist letter from Anthropic due to the name's similarity to its "Claude" model. The project was forced to rebrand to its current name, "Moltbot." During the transition, "bad actors" and "crypto grifters" took over the old, abandoned "Clawdbot" social media handles. These actors launched a cryptocurrency token on Solana ($CLAWDE), used the hijacked accounts to create the illusion of affiliation, and orchestrated a classic "pump and dump" scheme, driving the token's value to over $16 million before it crashed. This manufactured hype explains the significant gap between the tool's viral reputation as a consumer-ready "AI employee" and its reality as a risky, experimental project for technical users. 5. Security Considerations Beyond the hype lies a treacherous combination of practical risks. In its current state, Clawdbot / OpenClaw presents a dual threat of serious security vulnerabilities and an unproven return on investment, where the high cost and high risk are deeply intertwined. The security flaws are substantial. One analysis found "over 900 Clawbot instances with no security," leaking API keys and private chat histories. The project's creator, Peter Steinberger, issued a direct warning about its experimental nature: "yes most non-techies should not install this it's not finished i know about the sharp edges it's only 3 months old." This security nightmare is compounded by its cost structure. Unlike a flat subscription, the tool runs on API calls, which can become expensive quickly. One user reported spending "$300 on just the last two days" on API fees, and even enthusiast Alex Finn warned of hitting usage limits on a $200/month plan. This creates a perilous ROI calculation: you're paying high, unpredictable costs for a tool that could simultaneously expose your private keys and sensitive data. Analyst Nate Herk contrasts this with the more established Claude Code, which has "actual receipts" and proven ROI for shipping products. Clawdbot / OpenClaw, he argues, is currently driven more by "cool use cases" and "conceptual" hype, with little hard data on its actual business value. Having said all those negative things, it is still possible to install and operate OpenClaw in a secure manner and that is exactly what we do for our clients at Futureu Strategy Group. Who Is This For (and Who Should Stay Away)? Synthesizing the user experiences and expert warnings reveals a clear picture of the ideal user profile. This is not a tool for everyone. This tool IS for: Technical Founders, Indie Hackers, and Solopreneurs: As Alex Finn’s experience shows, those who can manage the technical setup and are looking for maximum leverage are the primary audience. Security-Savvy Tinkerers and Hobbyists: Nate Herk’s analysis identifies users who are "comfortable running a server, wiring APIs, thinking about ports, privacy, [and] blast radius." Power Users and Developers: Those who understand the risks and want to experiment with the future of autonomous AI agents will find it a compelling sandbox. This tool IS NOT for: "Most non-techies": A direct warning from the project's creator, Peter Steinberger, who emphasizes that the tool is unfinished and has "sharp edges." Anyone handling sensitive personal or client data: The security risks of exposing API keys and private information are currently too high for production use in secure environments. Users seeking a simple, plug-and-play productivity app: The extensive onboarding and technical setup required are far from a consumer-ready experience. A Glimpse of the Future Ultimately, Clawdbot / OpenClaw serves as a powerful proof-of-concept, not a production-ready tool. The proactive, autonomous capabilities demonstrated by users are an exhilarating glimpse into a future where everyone might have a dedicated digital employee. For the security-conscious developer or dedicated hobbyist, it’s a thrilling sandbox for the future of AI agents. Many of our clients report high levels of productivity from their OpenClaw agents and could not do without their agents. When deployed safely, the rewards are worth the risks. (this article was first published by the author in his newsletter at www.Onemorethinginai.com)

Nano Banana Pro Review: AI Image Generation and Visual Content Creation Tool Tested